With the national health emergency associated with the COVID‑19 pandemic in its third year, the financial health of independent anesthesia groups and healthcare organizations employing anesthesiologists is being firmly tested. Procedure volumes for many health systems remain below historical levels for numerous reasons, including staffing shortages that have reduced OR capacity and lingering patient hesitancy about the safety of various care settings.

However, many of the financial and operational trends negatively impacting the financial viability of these groups started long before COVID‑19. These trends include:

- Rising salary expectations for providers.

- Increased coverage requirements at times and in settings that are less efficient for anesthesia production

- Poor Medicare reimbursement rates relative to other specialties.

And for some groups, that list now includes the No Surprises Act, which took effect on January 1 and restricts professional billing from out-of-network providers at in-network facilities. While many organizations have already eliminated balance billing, the act still hinders independent groups working within a major system when negotiating with commercial payers because they must avoid any scenario resulting in them going out of network. This consumer-oriented move is advantageous for healthcare systems, but it comes at a precarious time for independent hospital-based groups.

Physician and CRNA Compensation Trends

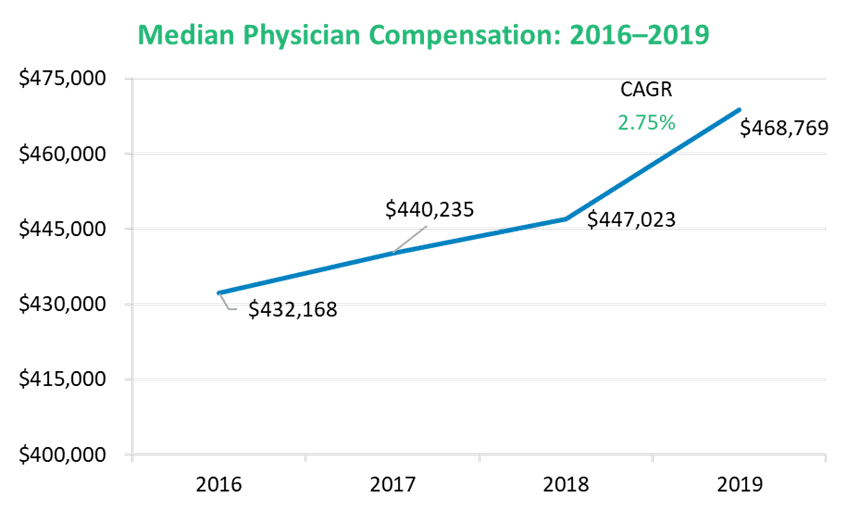

Compensation benchmarks have been materially impacted by the pandemic, rendering data collected in 2020 and 2021 less reliable than normal. Some anesthesia groups benefited from supplemental funding from the Paycheck Protection Program (PPP) in 2020, while others received additional funding from their partner health systems to help survive the financial impact of the pandemic and keep the groups whole for when surgical volumes returned. But even with these measures, many groups were forced to cut pay during the pandemic. However, early looks at data collected throughout 2021 imply the dip is temporary and that the larger trendline that formed from 2016 to 2019 will continue unabated as volumes return.

Compensation for all anesthesiology providers and particularly for certified registered nurse anesthetists (CRNAs)[6/24/22, Anna H: I PLR’d the definition here to keep the heading above short.] has experienced an upward trend over the past five years. Physician compensation has increased steadily, while CRNA compensation has experienced a spike that grew even more pronounced throughout the pandemic as demand for lower cost coverage alternatives charged the market for CRNAs.

As more states permit CRNAs to practice independently, competition for their services has trended upward. Anesthesiologist-only practice models are increasingly rare as groups and organizations determine that a blended coverage model is the most cost-efficient model across a diversity of inpatient and ambulatory care settings. As shown in figure 1, CRNA compensation increased by 3.51% from 2016 to 2019, and many groups are reporting severe challenges with recruiting and retaining the number of CRNAs necessary to fill daily coverage requirements.

Figure 1: National Benchmarks—Anesthesiologist and CRNA Compensation per 1.0 FTE[1]

Coverage Model Trends

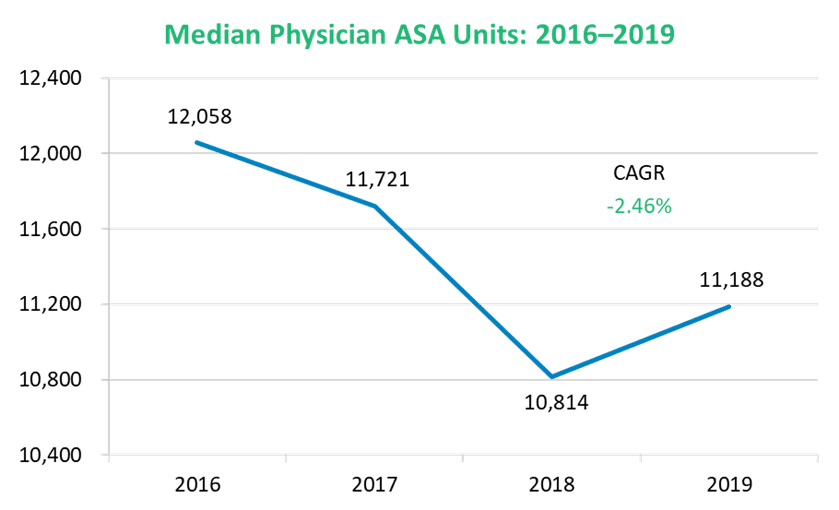

One of the most common challenges to the finances of anesthesia departments is the increased need to cover less efficient care settings, including evenings or weekends and at non-OR anesthesia (NORA) sites. This is reflected in production per FTE data, which trended downward from 2016 to 2019, as shown in figure 2.

Figure 2: Physician and CRNA ASA Units

It is helpful to think of anesthesia care settings in terms of “ASA density” (the number of ASA units generated in an hour of coverage). A highly efficient ambulatory surgery center (ASC) is usually the most ASA-dense setting, because surgical cases can be efficiently scheduled and operational factors such as late starts and room turnover are minimized. This is juxtaposed against a high-acuity setting like a heart hospital, where it is possible that only one or two cases are scheduled each day, or a trauma center with open surgical capacity. When surgical cases have less easily projected durations, or the presence of learners creates elongated cases, additional slack is required in the scheduling templates. This impact of this is illustrated in figure 3.

EXHIBIT III: Operational Optimization—Impact of Base ASA Units

There are additional factors at play, including the demand for anesthesia coverage at NORA sites and the proliferation of surgical “flip rooms,” where a single surgeon is given access to two ORs, a scenario that maximizes the surgeon’s efficiency at the expense of the anesthesia team’s efficiency. These additional coverage requests often make financial sense for a health system—flip rooms are a major satisfier for surgeons and maximize their capabilities, while services conducted at NORA sites are less invasive, utilize technology advancements, and help reduce overall system costs—but their impact on the financial performance of anesthesia in isolation should not be ignored.

Professional Reimbursement Trends

Beyond the challenges of rising provider costs and less efficient coverage settings that anesthesia groups and departments currently face, Medicare reimbursement for anesthesia remains stubbornly low when compared to other specialties. One simple measure of this is to multiply the median ASA production benchmark for anesthesiologists by the CMS reimbursement rate and compare that to the median compensation benchmark. This calculation of reimbursement as a percentage of compensation is among the lowest across all medical and hospital-based specialties, which creates additional pressure for medical groups to rely on commercial reimbursement to make up the difference.

However, many large multispecialty medical groups must determine a delicate balance of give and take across specialties when negotiating with commercial payers, and anesthesia is rarely prioritized. This only exacerbates the losses realized by the departments. For smaller, localized independent anesthesia groups, the No Surprise Act can undermine their negotiating position with commercial payers, making them increasingly reliant upon their system partnership agreements to remain financially viable.

Looking Ahead

Organizations employing anesthesiologists and CRNAs should be aware of the increasing cost per room for all anesthesia services under every coverage model. This is among the reasons to ensure the perioperative team is efficiently scheduling procedures and maximizing OR capacity. Organizations should know the cost to the system of adding or extending ORs or opening NORA sites. While the increased capacity is likely clinically necessary, understanding the incremental investment (or loss) sustained by the anesthesia department will drive more informed decisions.

For independent anesthesia groups to maintain long-term financial health, they should attempt to achieve a “portfolio” strategy, whereby they pursue arrangements with numerous system partners across an array of inpatient and ambulatory settings. This strategy avoids overreliance on a single partner, hedges against OR staffing challenges beyond the group’s control, and can reduce the call burden for the group, since ASCs usually represent the most efficient setting, have a better payer mix, and have no call coverage obligation.

Finally, independent groups should consider allowing CRNAs to take an equity stake in the group or an operational leadership role. There is inherent instability for smaller independent groups, where the loss of a single provider can diminish coverage capacity and necessitate the use of high-cost locums, a cost often incurred by the group. Many smaller groups are finding it harder to recruit, as risk-averse new graduates seek the stability of larger practices or system employment, and this creates challenges to long-term succession planning. As smaller groups survey the healthcare landscape to gauge their viability against the broader macro-market pressures described above, these short- and long-term challenges should factor heavily in their risk mitigation strategies and their vision for the future.

Authors: Clark Bosslet, Shelby Jergens – Contributor: Dave Wofford – ECG Management Consultants

[1] Based on a median respondent-weighted blended benchmark of MGMA, ECG, and AMGA data, and years are based on data collection period for anesthesiologists